Tariffs and Trade Post-SCOTUS Ruling

What happened? On February 20, the Supreme Court ruled that revenue could not be collected from tariffs imposed last year under the International Emergency Economic Powers Act (IEEPA). President Trump moved quickly on a replacement plan, starting with a 10% tariff announced on the same day as the ruling and then moving that to 15% the next day (that level remains in place as of this writing on February 23). We calculate that the 15% rate plan amounts to a $70 billion reduction in tariffs relative to IEEPA on a 12-month basis. This fits with our thinking that the question was not “if” but “how” the president had tariff authority to impose tariffs. Last June we outlined the following two-step plan that could be used to reimpose tariffs in the event of SCOTUS ruling against the IEEPA usage:

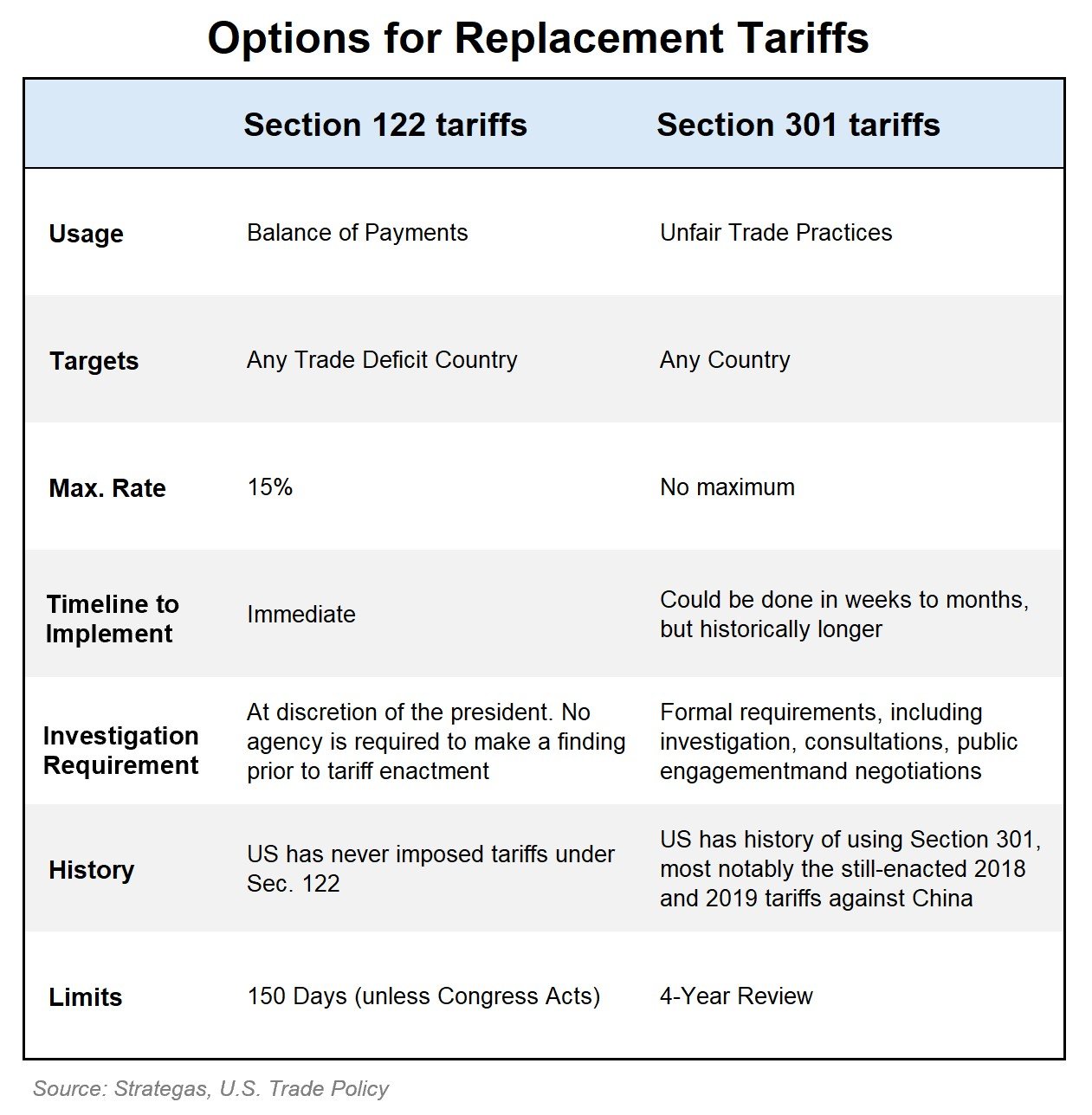

Step 1: Invoke Section 122 of the Balance of Payments Act as a temporary replacement to the IEEPA tariffs with a 15% tariff rate. These tariffs can remain in effect for 150 days. The new rate is a tariff cut for many countries, and will be most impactful for countries with tariff rates closer to 20% (e.g., Asian supply chain countries). Canada and Mexico are exempt from the 15% rate. This is consistent with our view that USMCA countries are the biggest relative winners from this administration’s trade policies. (Notwithstanding looming USMCA negotiations, Mexico and Canada have been exempted from larger tariffs, encouraging supply chains to locate in the North America region.)

Step 2: While the 15% tariff rate is in place, the White House can impose new tariffs through Section 232 (sectoral tariffs for national security) and begin investigations for Section 301 tariffs. Though Section 301 investigations take time, the policy pathway allows for unlimited tariff rates. The administration has known that the IEEPA tariffs could be overturned and has likely been strategizing ways to bundle countries together and expedite the review process. The 2018 Section 301 review on China could be used today if the administration wanted to, allowing immediate tariff hikes on China. Section 301 is a well-established authority for the executive branch and provides more certainty regarding tariffs given its stronger legal standing.

Refunds? We do expect tariff refunds, although the process is murky. We estimate that $130 billion of tariffs paid could be subject to a refund, but the Supreme Court did not address the issue. Our base case is that the Court of International Trade (CIT) will move quickly on the refund process. However, we don’t believe CIT has the authority to force U.S. Customs to rebate all claims. We expect this to be fought out in the courts with a legal process likely needed to outline the process.

SCOTUS decision summary. Chief Justice Roberts wrote the Court’s 6-3 majority opinion that the executive branch does not have authority under IEEPA to impose tariffs, noting that the authority to tariff is a taxing power which is a different type of authority than others outlined in IEEPA. Chief Justice Roberts also stated that Congress could have explicitly provided tariff authority under IEEPA if it had wanted the president to have it. Further, he stated that the precedents given for using IEEPA to impose tariffs did not hold up and that there is no exception from major questions for emergency statutes or for foreign affairs. Justice Kavanaugh’s dissent, in which he was joined by Justices Alito and Thomas, pushed back on assertions in the majority opinion and pointed to other trade authorities by which the IEEPA tariffs could be replicated. The majority opinion did not address the question of refunds and no process was laid out for how that issue should be resolved. In his press conference after the ruling, Trump said that refunds would likely need to be litigated. We’ll have to see how the legal process unfolds, but over 1,000 cases are currently sitting at the Court of International Trade on this. This could very well end up on the Supreme Court’s docket.

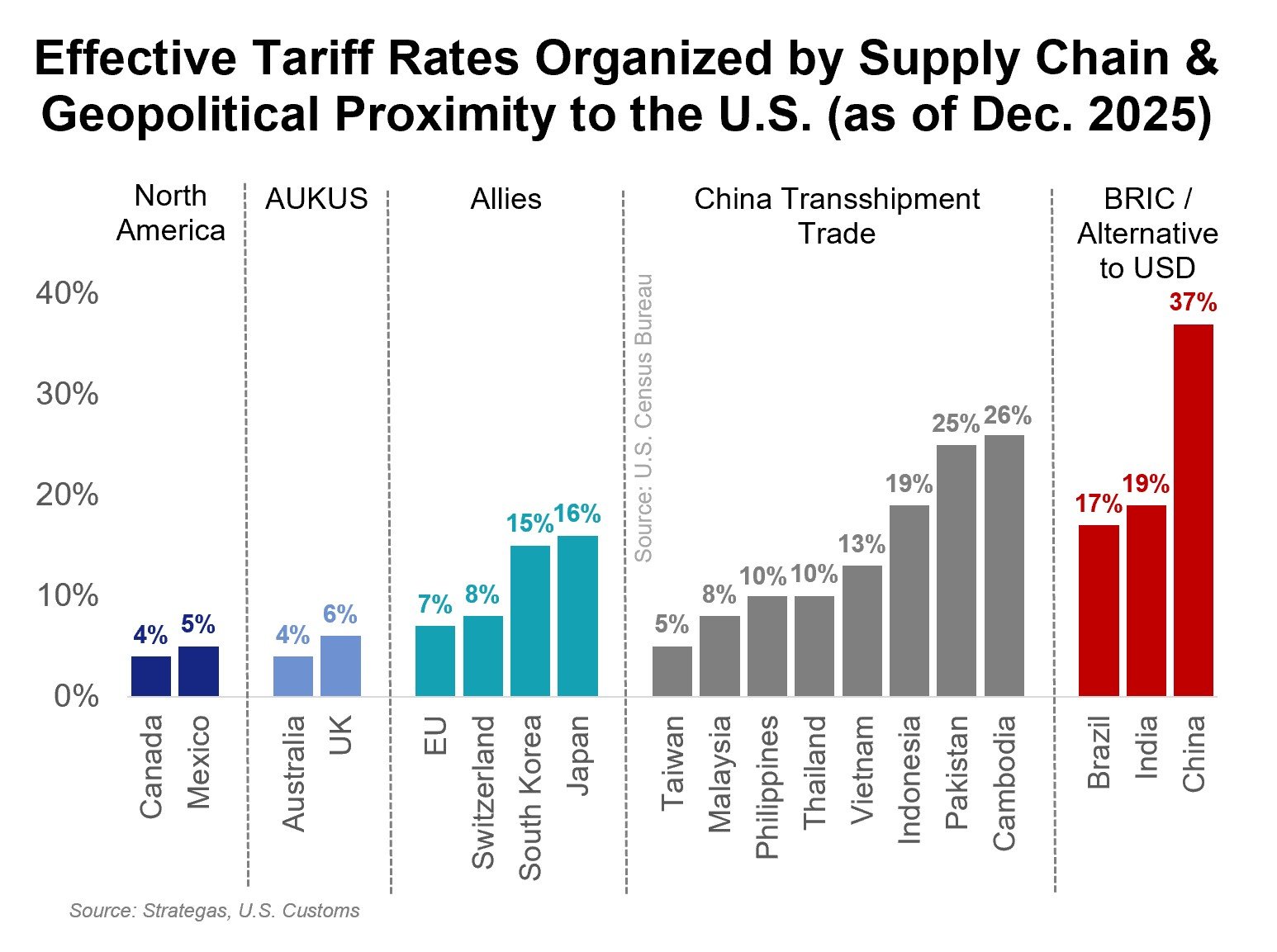

USMCA and trade deals. USMCA-compliant goods will remain exempt from the 15% global rate that was issued after the Supreme Court ruling. Canada faced a 35% tariff rate under the fentanyl IEEPA tariffs and Mexico faced a 25% rate. But because USMCA goods were exempt from the tariffs, along with lower rates on select goods categories, the effective rates were dramatically lower. As of November 2025, Canada had an effective tariff rate below 4% and Mexico had a rate below 5%. More broadly, USMCA’s upcoming review (in July) has looked increasingly contentious after Prime Minister Carney’s deal with China and speech at the World Economic Forum. There was already a growing and complicated list of issues for the review, including AI, critical minerals, Arctic security, rules of origin, and energy reforms. A few possibilities for what could happen in July include the following:

- Agreement on 16-year extension without major changes (very unlikely, in our opinion)

- Renegotiation of USMCA with long-term extensions (both unlikely and difficult, in our opinion)

- Renewal of USMCA with side letters used to address changes for long-term extension

- Reversion to annual reviews after no unanimous agreement on a 16-year extension

- Withdrawal of the U.S. from USMCA (requires 6-month notice) and a move to bilateral deals.

The U.S. is increasingly discussing bilateral deals, but the tone has shifted. In December, U.S. Trade Representative Greer noted that the US had better relations with Canada than Mexico, and that that should be the bilateral pursuit. But post-Davos speech and post-China deal, the U.S. has threatened to pursue a bilateral deal with Mexico and leave Canada out.

Tariff watch continues. Although legal issues have shifted in the background and the details of White House trade priorities continue to shift in the foreground, the recent Supreme Court ruling is just one more development in the long and bumpy story of trade policy since Trump took office last year. Our team will continue to monitor new wrinkles as they arise; in the meantime. we remind Baird clients to reach out to their Baird advisors with any questions related to their own portfolio and circumstances.

APPENDIX – IMPORTANT DISCLOSURES

Past performance is not indicative of future results. This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent.

This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. Unless otherwise cited, market and economic statistics come from data providers Bloomberg and FactSet. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry or security. Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client. Investment involves risk. You should review the prospectus or other offering materials for an investment before you invest. You should also consult with your financial advisor to assist you with your analysis, risk evaluation, and decision-making regarding any investment.

The performance and other information presented in this communication is not indicative of future results. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies. Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication.

Strategas Securities, LLC is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses. A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at https://www.rwbaird.com/research-coverage/. You can also call 1-800-792-2473 or write: Baird PWM Research & Analytics, 777 East Wisconsin Avenue, Milwaukee, WI 53202.