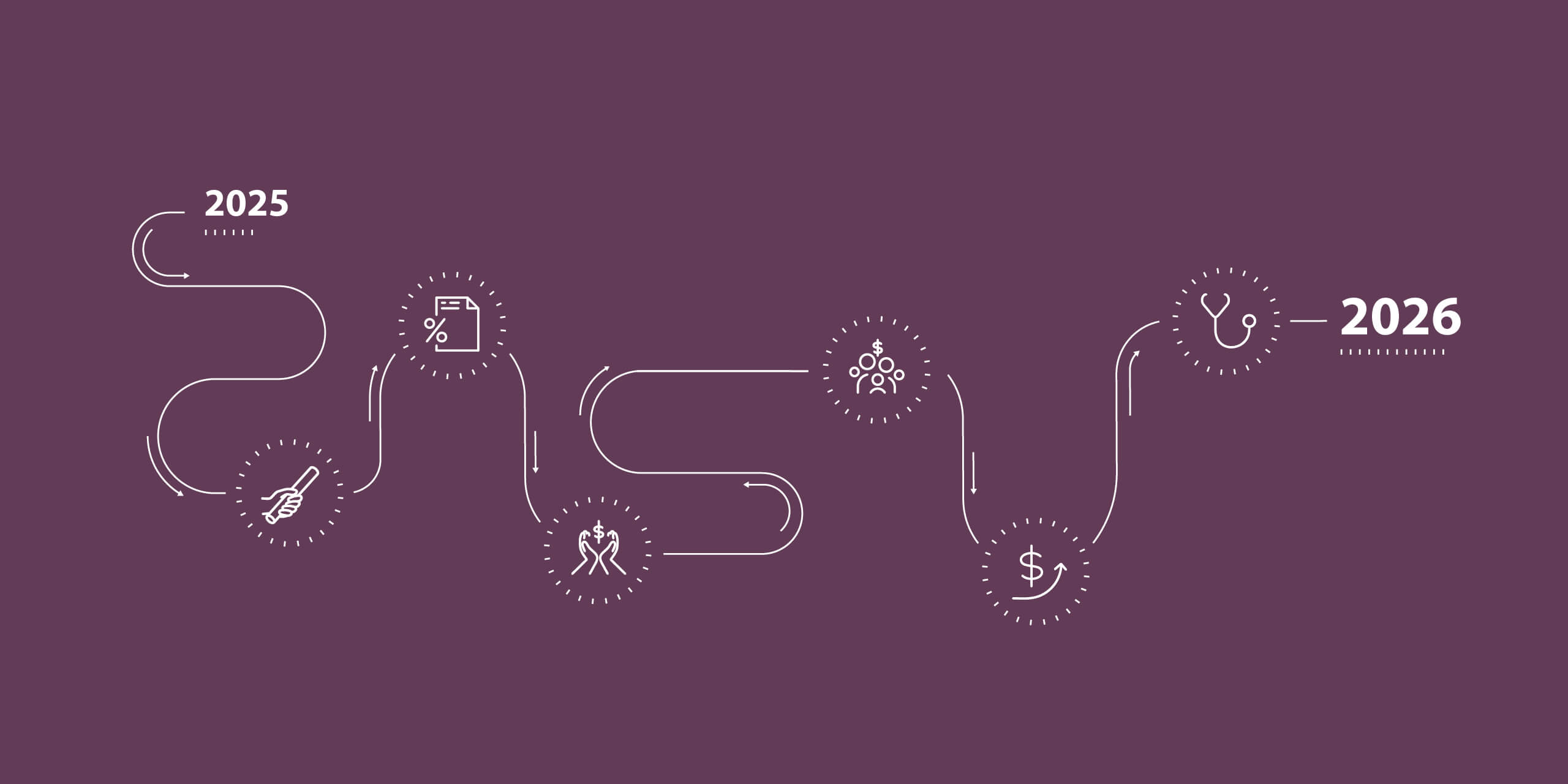

2026 Planning Moves: What’s New and What To Watch

While every year brings new updates to tax rules and retirement savings plans, 2026 stands out with several fresh provisions and opportunities in the way of the One Big Beautiful Bill Act (OBBBA).

Here’s how to make the most of what’s new – and plan for what’s coming – in each of the following core planning areas.

Preserving Your Legacy

In the summer of 2025, the OBBBA permanently increased the lifetime gifting and estate tax exemption. Before the bill, it was set to drop to around $7 million in 2026 – but now, the exemption has been increased to $15 million. This expanded exemption creates new opportunities to support loved ones and leave a lasting impact while staying tax-efficient. Now is the time to connect with your advisor team and explore whether revisiting your estate plan and gifting strategy could help bring your long-term goals to life.

Staying Ahead of New Tax Hurdles

Tax planning should stay in focus in 2026, as the OBBBA lowered the income threshold for the Alternative Minimum Tax (AMT). Starting this year, more taxpayers – especially those earning over $1 million – may find themselves subject to the AMT. Additionally, itemizers will now see the tax benefit of deductions capped at 35%. Reviewing your most recent tax return with your advisor team can help you avoid surprises come the 2027 tax season.

Making an Impact Through Giving

Recent changes to charitable giving rules make it even more favorable to plan your donations strategically. For those claiming the standard deduction, an extra deduction is available for cash gifts made to public charities (excluding private foundations or donor-advised funds). Joint filers can claim up to $2,000, and single filers up to $1,000.

For itemizers, new restrictions on deductions apply. Only charitable contributions exceeding 0.5% of adjusted gross income will be deductible. Your advisor team can help coordinate your giving to maximize your tax benefit and philanthropic impact.

Caring for Your Family

Expanded benefits are now available for working parents, including an increased child and dependent care tax credit of up to 50% of qualifying expenses. Revised phaseout rules maintain the 20% floor, meaning even families with higher incomes may still qualify for part of this credit.

Enhanced investment opportunities are also emerging for families. For one, 529 accounts continue to become more flexible – doubling the amount beneficiaries can use on K-12 tuition and other expenses to $20,000. In addition, the OBBBA introduced Trump Accounts: a new type of savings account for children under age 18, launching this July. These accounts allow up to $5,000 in annual contributions to help jumpstart children’s saving journeys. Rules and restrictions apply, so check with your advisor team to see how these may fit your overall strategy.

Optimizing Your Business Income

This year, owners of pass-through businesses (like LLCs or S corporations) can still exempt part of their income from tax under the Qualified Business Income rules – and the phaseout range has expanded slightly, allowing even more owners to qualify. Additionally, 2026 brings a new $400 minimum deduction for business owners with at least $1,000 of qualifying income.

Meanwhile, C corporations face a notable change for charitable contributions: Only contributions exceeding 1% of taxable income can be deducted. This makes it especially valuable to align your business’s giving with its broader tax strategy.

Coordinating Your Health and Wealth Strategies

While the OBBBA drove many wealth planning changes in 2026, there’s also another element on the horizon: Rising healthcare costs – like the ones anticipated in 2026 – can put real pressure on even the most well-built wealth plans. The good news? With a little planning, your health and wealth strategies can work together to protect your future. Below are key action items to take with your advisor team for different stages of life:

- Working individuals: Choosing a high-deductible health plan can help offset rising costs by qualifying you for a Health Savings Account – where you can save pre-tax dollars for future medical expenses.

- Pre-retirees: Proactively exploring long-term care insurance and other protective strategies can help safeguard your retirement income from higher care costs.

- Those approaching 65: Developing a Medicare cost projection and choosing the best plan option for your needs can help you prepare for expected Medicare cost hikes.

- Everyone: Prioritizing preventative care will help you stay healthy longer, reduce future medical costs and stay focused on building and enjoying your wealth.

The evolving rules of 2026 serve as a reminder of the everchanging landscape. By staying informed and working closely with your advisor team, you can continue to adapt your wealth strategies to safeguard your financial future.

This information has been developed by a member of Baird Wealth Solutions Group, a team of wealth management specialists who provide support to Baird Financial Advisor teams. The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. The information reflected on this page are Baird expert opinions today and are subject to change. The information provided here has not taken into consideration the investment goals or needs of any specific investor and investors should not make any investment decisions based solely on this information. Past performance is not a guarantee of future results. All investments have some level of risk, and investors have different time horizons, goals and risk tolerances, so speak to your Baird Financial Advisor before taking action.