In the Markets Now: King Cash (and False Security)

Cash can offer perceived safety, flexibility, and short‑term stability but the purchasing power of excess cash quietly erodes over time.

Security

In response to the devastating impact of World War I, France spent the early 1930s building an extensive network of concrete bunkers, artillery casemates, and underground tunnels – the Maginot Line – to prevent a repeat of WWI–style trench warfare and deter German invasion. Today, however, the Maginot Line is known better as an example of perceived safety contributing to a poorer outcome down the road. Fair or not, many historians have concluded that the presumed strength of the line anchored French military planning to the assumption that its borders were secured, fueling underinvestment in mobility, flexibility, and other defenses. When Germany reoriented its approach around speed and surprise, “blitzkrieg” tactics, the line was simply bypassed. In a sense, it did not just fail to stop the invasion, it left the country more exposed than if it had remained “uncertain” and more adaptable. The Maginot Line has since come to embody the risks of a false sense of security.

Cash

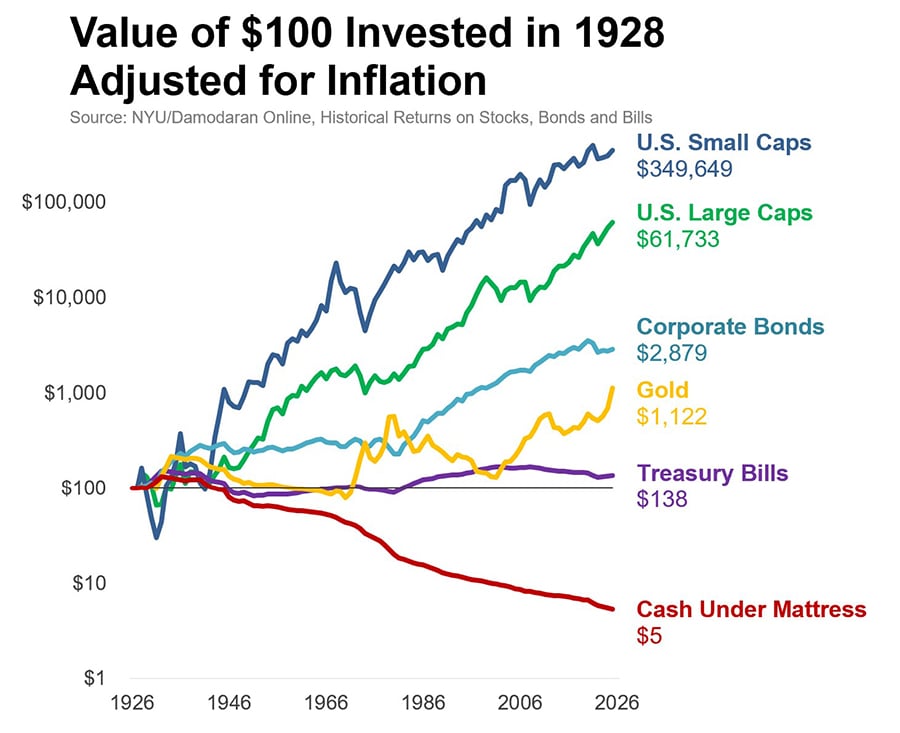

As I was reading about the Maginot Line, my investing brain couldn’t help but think of examples of this in portfolios – perceived security obscuring, and perhaps contributing to, a more existential but less obvious risk. My mind went immediately to our love of cash. Holding cash definitively feels more certain than investing in the stock market because its value is nominally stable – one dollar today is still one dollar tomorrow. Unlike stocks (or bonds, gold, etc.), cash does not fluctuate in price, respond to worrying headlines, or require investors to stomach short‑term losses. This creates a strong sense of psychological safety, especially during periods of economic uncertainty or political unrest. However, this comfort is a wolf in sheep’s clothing... while cash minimizes visible volatility, it quietly exposes investors to inflation risk, steadily eroding purchasing power over time.

Yields

This is particularly timely today because in recent weeks, expectations that the Federal Reserve will deliver two or more 2026 interest rate cuts have increased, sending short-term interest rates to multi-year lows. For most investors, this is largely a positive. Higher rates increase borrowing costs, weigh on stock market valuations, and render bonds a more attractive alternative. Even in this bull market, higher rates have been a thorn in investors’ side. Fed cuts ease those pressures. But lower interest rates come with a price, too – when the Fed cuts rates, yields on cash‑like investments (e.g., money market funds) generally fall – and quickly. This is a big risk as assets in money market funds have skyrocketed from under $3 trillion in 2017 to nearly $8 trillion today. Higher yields in recent years have attracted investor dollars to cash-esque products like moth to flame, but as rates continue to fall (and with inflation a bigger concern today than it’s been in decades), much of that sidelined “cash” could likely do with a better home.

Tool

Of course, cash has its place. It provides a combination of liquidity, flexibility, and risk control benefits that other assets typically don’t offer. As the author Morgan Housel writes, “cash is the oxygen of independence.” But while that may be true, cash is not a wealth-building tool and holding excess cash instead of investing it increases your risk of falling short of longer-term goals (just ask Warren Buffett, who wrote in the depths of the 2008 Crisis that “today people who hold cash equivalents feel comfortable. They shouldn’t. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value”). Peace of mind is important, but so is participating in long‑term wealth creation.

Disclosures

Investors should consider the investment objectives, risks, charges and expenses of any fund carefully before investing. This and other information about a fund can be found in the prospectus or summary prospectus. A prospectus or summary prospectus may be obtained from your financial advisor or the fund website and should be read carefully before investing.

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2026 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.