Key Takeaways from Strategas Research Areas

Strategas provides a comprehensive snapshot of current market and economic conditions through their eight research areas.

May 18, 2026

Investment Strategy

Jason Trennert, Chief Investment Strategist and Chairman

The major building blocks of employment, financial conditions and corporate profits all tilt toward a continuation of the bull market.

Spending boom. The AI trade is real, and the capital spending boom is likely to continue. The CEOs of the biggest AI-related companies are at more career risk if they don’t invest heavily in AI than if they do and lose money. The provisions of the One Big Beautiful Bill provide further incentive to keep spending. Based on consensus estimates, Microsoft, Amazon, Google, and Facebook will only have $4 billion in free cash flow by Q3. A greater reliance on the debt markets may be necessary to sustain the growth in capital spending.

Spending boom. The AI trade is real, and the capital spending boom is likely to continue. The CEOs of the biggest AI-related companies are at more career risk if they don’t invest heavily in AI than if they do and lose money. The provisions of the One Big Beautiful Bill provide further incentive to keep spending. Based on consensus estimates, Microsoft, Amazon, Google, and Facebook will only have $4 billion in free cash flow by Q3. A greater reliance on the debt markets may be necessary to sustain the growth in capital spending.- Earnings soaring. Corporate profits remain supportive of the bull run; Q1 S&P 500 profits were up +28.6% year over year.

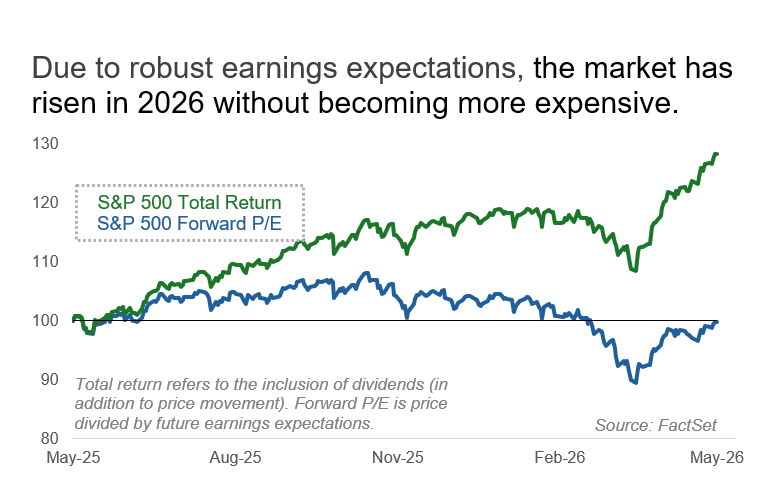

- Valuations rich. Valuation tends to be a poor timing tool, but the market has been expensive by almost any historical measure: trailing P/E, forward P/E, EV/Sales, EV/EBITDA, Price/Book, Price/Sales, etc. However, strong earnings have led to multiple compression in 2026, allowing the market to rise without becoming even more expensive.

- AI vs. Iran. Excitement over AI is more than offsetting concern about the war with Iran, despite the changeable nature of commentary on the prospect of the Strait of Hormuz re-opening.

- Yields on watch. We see early signs of inflation and the recent rise in 10-year Treasury yields as the biggest risks to the bull market. Over the past four years, a 10-year Treasury above 4.5% has been a tough environment for the market. We expect Inflation expectations (stable for now) to determine monetary policy at the Fed.

- Investment themes. Our major investment themes remain 1) Cash Flow Aristocrats; 2) Artificial Intelligence; 3) the Industrial Power Renaissance; and 4) Deglobalization.

Asset Allocation

Nicholas Bohnsack, President and Head of Portfolio Strategy

Strategas has ramped up exposure to alternatives in response to changing markets.

- Portfolio construction. Over the past several years, we slowly increased exposure to Gold and other metals. We believe an incremental adjustment to a 60/30/10 (stocks/bonds/alternatives) framework is prudent given structural impact on client portfolios. Recent volatility in metals markets stands case in point.

- Energy in focus. Energy remains the primary link between geopolitics and investment outcomes. We remain focused on evolving pockets of momentum in our research, but disruptions at Hormuz extend beyond oil. Fertilizer shortages could reduce agricultural output, supply chain issues could increase manufacturing costs, and freight blockades and insurance limits could widely constrain logistics.

- Where we stand. Last month we reduced our broad Equities allocation to slightly Underweight from Neutral – relative to both a traditional 60/40 benchmark and our preferred 60/30/10 baseline which includes an Alternative sleeve. Within Equities we maintain a slight Overweight to U.S. shares, achieving a gross Underweight by reducing exposure to Developed Markets. We have reallocated the reduced Developed Market exposure between Emerging Market equities and direct exposure to the agriculture sector within the Alternatives bucket.

Economics

Don Rissmiller, Chief Economist

We place the odds of a recession in 2026 at 35% (with 55% odds of solid growth and 10% chance of upside surprise).

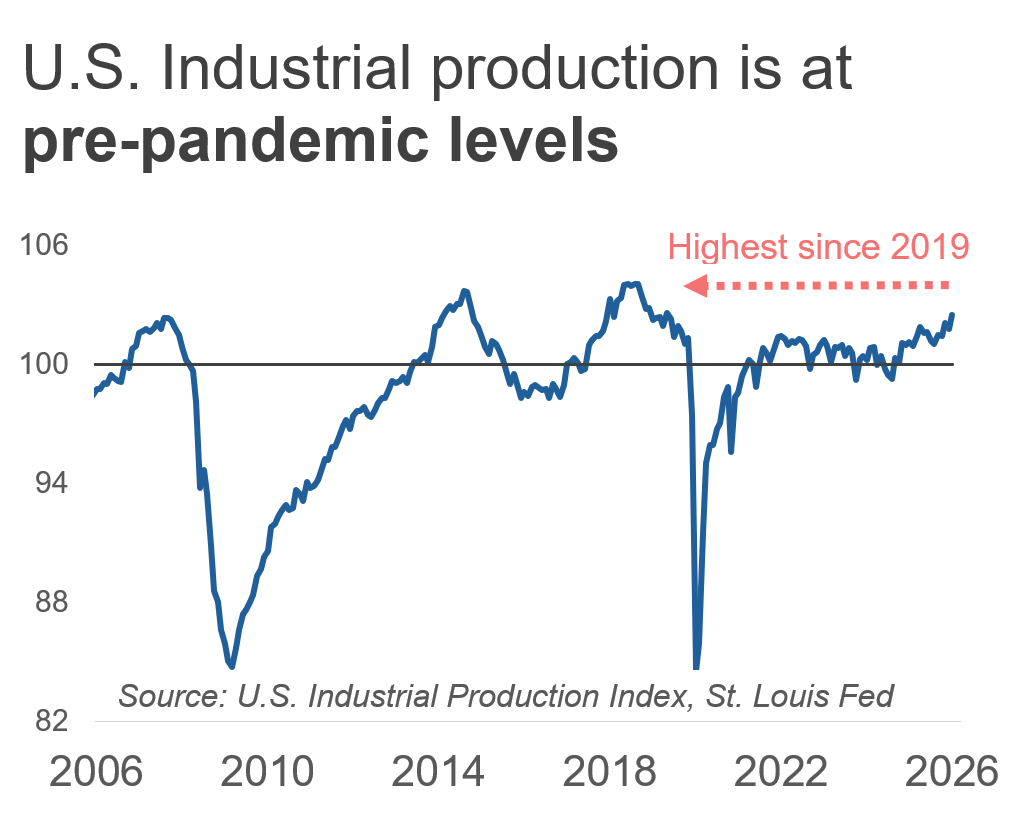

Growth. Fiscal stimulus for consumers has muted the impact of higher energy prices. If not for that shock, we could be talking instead about the U.S. economy reaccelerating due to cyclical sectors (e.g., manufacturing) improving. The AI capex story is a continued support.

Growth. Fiscal stimulus for consumers has muted the impact of higher energy prices. If not for that shock, we could be talking instead about the U.S. economy reaccelerating due to cyclical sectors (e.g., manufacturing) improving. The AI capex story is a continued support.- Inflation. The last wave of inflation peaked in 2022, and inflation expectations still look anchored. But history suggests that a second wave tends to build and given supply-chain interruptions in 2026, we may be seeing early signs of that. We’ll watch domestic rents and wages to gauge whether this pattern holds.

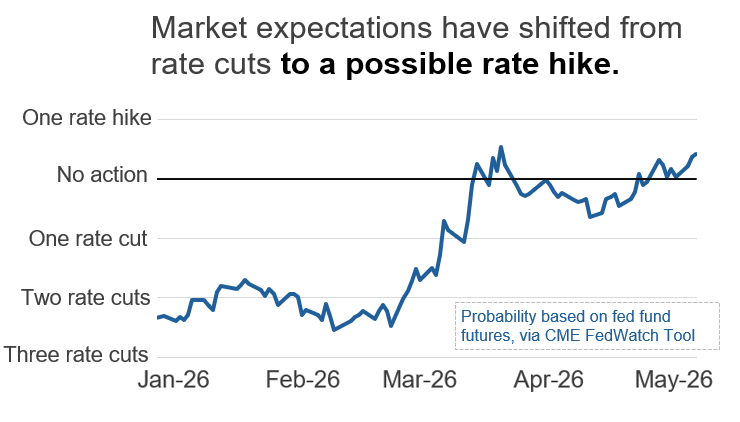

- Policy. 2024 and 2025 saw lower monetary policy rates, justified first by inflation coming down and reinforced by cracks in employment. The Fed looks to be on an extended pause. The textbook monetary policy response is to look through supply shocks, but that requires long-term inflation expectations to remain anchored.

- Risks. Fiscal supports that have aided growth have not been cost-free. While there’s no emergency, the federal budget deficit threatens to crowd out other economic activity. Fixing this abruptly risks an economic stop. Alternatively, inflation could return if expectations become unanchored due to repeated shocks. The market would likely demand higher interest rates in that scenario.

- Hope. Productivity can conceptually alleviate an inflation wave, as too much money chasing too few goods can be countered by producing more goods in the same amount of time. There is promise from tech advances, but we would like to see the profits of both the producers of AI and the users of that technology growing at the same time.

Technical and Market Strategy

Chris Verrone, Chief Market Strategist

“Melt-up” remains the call, though breadth and other macro headwinds are on watch.

- Base case:

- The trend for most global equity markets is intact (up and to the right) though participation has narrowed with just 53% of S&P 500 stocks in uptrends. We’re still playing but are starting to look over our shoulders. There’s temptation to compare this narrowing advance to 1999/2000 but we’re not in that category yet; at the March 2000 peak, only 27% of the S&P was in an uptrend.

- Whether your bubble analogue is 1989 Nikkei or 1999 Nasdaq, rates tend to run up near the end of the melt-up phase. Today, yields look like they want to break out but have not triggered credit weakness or the defensive leadership that often accompanies a late-cycle ending.

- We continue to prefer real economy industries / stocks, which are home to many of the market’s best trends. Meanwhile, Consumer Discretionary and Consumer Staples both remain in weak condition (this is still a capex cycle, not a consumer one).

- In particular, we continue to like Copper and basic resource stocks – Industrial Metals over Precious Metals, with confirmation from the Aussie dollar. We remain Japanese equity bulls.

- Risks to base case:

- Where can the 2-year yield go? We don’t think 4.50% is crazy. That would be a rude welcome for the new Fed chair, as rates globally look like they want to move higher.

- Banks not loving the flatter yield curve (i.e., the spread between short-term rates and long-term rates narrowing). Relative weakness among some big money-centers banks bears watching.

- Sentiment not quite in the danger zone yet but is getting closer as weaker seasonals (mid-July through mid-October) approach. Semiconductors are in the extreme zone (flows, volume, deviation from trend), along with South Korea and Taiwan. Managing risk here is prudent.

Questions on our mind: Why is the Real Estate sector improving (albeit modestly) even with rates hot? Can Memory / AI correct without our Basic Resource longs getting hit? Are we too complacent about what’s correlated to AI? Is Gold just a risk asset? How at risk is Gold with 2-year yields higher?

Washington Policy

Dan Clifton, Head of Policy Research

An Iran cushion in the form of stimulus, a test for a new Fed Chair, and midterm volatility building.

Rates outlook. A key theme for 2026 was “shock-and-awe” economic policy, featuring individual and business tax cuts, reduced tariffs, and financial deregulation. That stimulus was set to accelerate U.S. growth but is now serving as a cushion against higher oil prices and other supply chain constraints. Although tax refund season has ended, companies will continue to benefit from business investment incentives in the OBBB passed last July, and importers will receive approximately $100bn in IEEPA tariff refunds. If Iran is not resolved in short order, consumers will feel the squeeze; policymakers are proposing new stimulus measures ahead of the midterms as a result.

Rates outlook. A key theme for 2026 was “shock-and-awe” economic policy, featuring individual and business tax cuts, reduced tariffs, and financial deregulation. That stimulus was set to accelerate U.S. growth but is now serving as a cushion against higher oil prices and other supply chain constraints. Although tax refund season has ended, companies will continue to benefit from business investment incentives in the OBBB passed last July, and importers will receive approximately $100bn in IEEPA tariff refunds. If Iran is not resolved in short order, consumers will feel the squeeze; policymakers are proposing new stimulus measures ahead of the midterms as a result.- Lingering conflict. The U.S. and Iran are in a stalemate, with Iran seeking to control traffic through the Strait of Hormuz and the U.S. seeking to block ships from going into or out of Iranian ports. A quick deal remains elusive, as both countries think economic pressure will cause the other to fold first. While negotiating positions have moved closer, a build-up of economic pain will likely force a change.

- A tough environment for a new Fed chair. Kevin Warsh will face a polarized Fed Board, with the regional Fed presidents making it clear that they do not support rate cuts. In addition, Powell will stay on as Fed governor. Our sense is that he is worried that relinquishing his seat would allow Trump to replace regional Fed presidents (which would allow the Warsh Fed more influence to shift policy toward a lower balance sheet and lower rates in 2027). Powell could stay on through the election in November; if Democrats take the Senate, that would limit who Trump could get confirmed as a Fed nominee.

- Democrats remain in the midterm driver’s seat. Democrats continue to outperform in special elections since the beginning of Trump’s second term. They have outperformed by an average of 11 percentage points relative to the prior elections in those districts and flipped seats in Republican strongholds (TX, FL, GA, IA, and AR). That shift in the electorate is consistent with a loss of 27 House seats for the GOP and puts Republican-held Senate seats in play. Efforts at midcycle redistricting will mitigate Republican losses but may not overcome Democratic momentum. Democrats need just a net three seats take control of the House. In the Senate, Democrats need to win a net four seats.

Equity Derivatives

Brandon Kobelt, Head of Equity Derivatives Research

- Breadth. This breakneck equity rally is one of significant dispersion at the index level, with Mag. 7 and AI-related stocks, especially Semiconductors, driving the bulk of gains. The Q1 earnings season has brought a second wind to the rally. Semiconductor stocks benefited from strong quarterly results and elevated call option activity.

- Dispersion. Semiconductors are now more than 18% of the S&P 500, and with the sector’s recent out-performance, leveraged funds in that space are increasingly popular. Because leveraged ETFs must rebalance daily, typically buying into rallies and selling into declines, this popularity has amplified volatility across the Semiconductor space and in large-cap indexes.

- Volatility. The recent call option demand has led implied volatility skew (the difference between downside put volatility and upside call volatility) for both index and single stocks to the steepest level since Oct. 2025, when the post-“Liberation Day” rally started to lose momentum. Trying to call a top is dangerous – what looks extreme today can become more extreme tomorrow – but today’s calls vs. puts set-up makes protective strategies (e.g., collars: selling upside calls to finance protection via downside puts) a potentially compelling overlay.

ETF Research

Todd Sohn, Chief ETF Strategist

- Enthusiastic inflows. Equity ETFs are averaging over +$6 billion in inflows per day since the March low, reflecting reengagement. Still, trailing 3-month flows are in their 70th percentile, suggesting room for more participation.

- Semiconductors are aggressive. If there is one area that stands out for aggressive behavior, it’s the Semiconductors. ETF activity – both levered and unlevered – has exploded. Taiwan has taken the mantle of largest allocation within Emerging Market benchmarks. The tentacles of Semiconductors extend to Industrials, where broad sector ETF and Infrastructure exposures have also seen significant inflows. Ten Space ETFs launched in the last three months (multiple ETF launches within a similar theme can be a red flag). We’d consider each of these a sentiment risk for the sector as Q2 progresses.

- Energy has cooled. As for Energy, both flows and volumes have cooled over recent weeks, while volatility vs. the broader market has collapsed. In an environment where traditional Defensives (Healthcare, Staples) have struggled, Energy – and Natural Resource ETFs overall – could serve as a path for investors to diversify their large-cap Growth exposure.

Fixed Income

Tom Tzitzouris, Head of Fixed Income Research

- Rinse and repeat. If it seems like we’ve been here before – not knowing if inflation is accelerating or declining, not sure if a recession will hit or if more stimulus will arrive to keep the consumer afloat for another 24 months – you’re not imagining it. We will likely be here again in 24 months, and the lesson we’ve learned since 2010 is not to expect the worst-case scenario or the best-case scenario. Yet the economy manages to chug along. For the bond market, the next quarter is likely to bring more arguments in favor of curve steepening and more arguments in favor of wider spreads than tighter/stable spreads.

- Rates outlook. We anticipate that growth will stay strong enough to keep the Fed from easing before the third quarter, and inflation is likely to keep the debate between easing and hiking more balanced than it should be. But at the end of the day the Fed is more likely to have to ease by end of 2026 than to raise rates. We expect to see the 10-year Treasury yield revisit the 4.6% to 4.8% zone this year, but very briefly, before growth begins to fade and inflation pressures once again drift back down toward 3%. But 3% inflation might be the floor, not the average, and that means most of the yield curve could be above 4% for the entirety of 2026 and 2027, even without rate hikes.

- Credit spreads. Consistent with the stop and go economy over the next 12 months, we expect to see credit spreads wobble slightly higher between now and middle of 2026. Investment grade spreads should remain below 100 basis points (i.e., one percentage point) for the rest of Q2. A growth pickup in the middle third of 2026, along with one more rate cut, could keep the lid on credit spreads until the end of 2026. But we anticipate that as growth begins to slow late this year and rate hikes become more likely in 2027, that lid will be lifted and credit spreads will begin a late cycle march higher. Still, despite a rocky road, the most important pieces to the spread puzzle (earnings and liquidity) both point toward stable spreads at very tight levels for at least another quarter.

Definitions of valuation multiples mentioned: Trailing P/E: The company’s current stock price divided by its earnings per share over the last 12 months. It shows how much investors are paying for actual recent earnings. Forward P/E: The company’s current stock price divided by expected earnings per share over the next 12 months. It shows how much investors are paying based on projected future earnings.. EV/Sales: Enterprise value divided by revenue. This measures the value of the entire business relative to its sales. EV/EBITDA: Enterprise value divided by EBITDA (earnings before interest, taxes, depreciation, and amortization). This measures the value of the whole business relative to a common proxy for operating cash flow. Price/Book: Stock price divided by book value per share. It shows how the market values the company relative to its net assets on the balance sheet. Price/Sales: Stock price divided by sales per share. It shows how much investors are paying for each dollar of company revenue. All of these valuation multiples can also be applied to an index such as the S&P 500; in this case, the metric represents these statistics for all companies in the index in aggregate.

IMPORTANT DISCLOSURES

Investors should consider the investment objectives, risks, charges and expenses of any fund carefully before investing. This and other information about a fund can be found in the prospectus or summary prospectus. A prospectus or summary prospectus may be obtained from your financial advisor or the fund website and should be read carefully before investing.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index. Market and economic statistics, unless otherwise cited, are from data providers FactSet and Bloomberg.

This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. Unless otherwise cited, market and economic statistics come from data providers Bloomberg and FactSet. This communication does not constitute, nor should it be regarded as investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry or security. Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client. Investment involves risk. You should review the prospectus or other offering materials for an investment before you invest. You should also consult with your financial advisor to assist you with your analysis, risk evaluation, and decision-making regarding any investment.

Baird does not currently recommend the purchase of any cryptocurrencies, products that attempt to track cryptocurrencies, or cryptocurrency custodians. Baird does not custody Bitcoin or any other cryptocurrencies.

The performance and other information presented in this communication is not indicative of future results. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies. Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication.

Strategas Securities, LLC is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses. A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at https://researchdisclosures.rwbaird.com/. You can also call 1- 800-792-2473 or write: Baird PWM Research & Analytics, 777 East Wisconsin Avenue, Milwaukee, WI 53202.