In the Markets Now: Inspecting IPOs

Anticipation has been building as investors look toward several initial public offerings expected by the end of 2026, including some really big names. But what happens after the initial buzz wears off?

Coming into 2026, investors expected a boom year in initial public offerings (IPOs). There was (and is) a large backlog of late-stage private companies, a conducive macro environment (stable interest rates, solid economy), and healthy investor appetite for AI-adjacent growth stories. And while the war in Iran has curbed animal spirits to an extent, it still seems likely that the U.S. will see several widely anticipated IPOs by year-end (including the mega-sized offerings of Anthropic, OpenAI, and SpaceX).

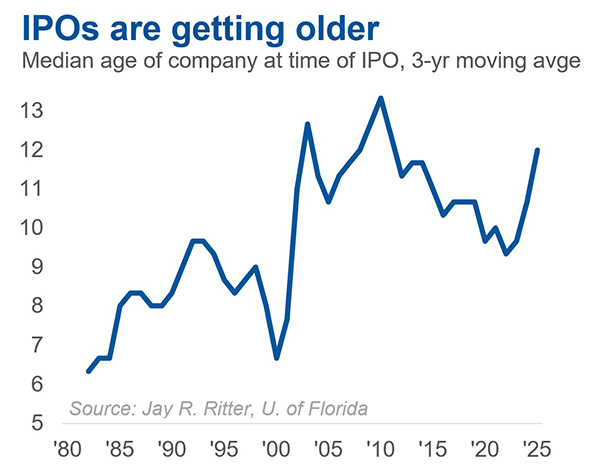

The size and name recognition of these firms (plus the cocktail party appeal of potentially owning them) puts the IPO market into a bigger spotlight than it has held for many years. Aside from the fact that the macro environment hasn’t been ultra-favorable to a booming IPO market (e.g., rising interest rates post-2021), there’s also the structural issue of companies staying private longer than they used to. There are many reasons for this trend. Private markets are deeper and more flexible than they used to be, liquidity options for private owners/employees are more available, and public companies have a higher regulatory burden than they once did. But it has impacted the IPO market and changed the dynamic for investors. IPOs today are often larger, more mature companies, which may be less risky investments than early-stage start-ups but it can also mean that a lot of the growth typically expected of a younger/newly public company is already baked into the valuation (i.e., the growth has already been captured by private investors before the public offering).

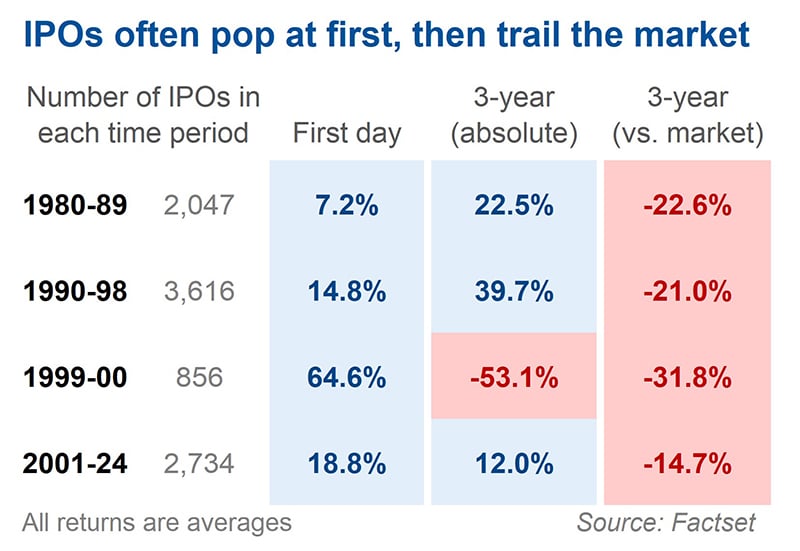

But what does history say? Is IPO hype warranted by performance? Typically, no. IPOs can lead to the occasional home run, but long-term returns have generally been poor. The average IPO (of nearly 10,000 IPOs since 1980) underperformed the market by over 20% in the first three years (measured from close of first trading day). Nearly 60% of these companies returned 0% or less over the three years that followed their IPOs.

Of course, no one expects IPOs to underperform. The average first day return for that same group of 10,000 stocks was nearly 20%. And the greater the hype, the bigger that initial pop can be. Of the nearly 1,000 IPOs that feel within the peak dotcom euphoria of 1999-2000, the average first day return was 65% (while the average 3-year buy-and-hold return was -53%). More recently, the SPAC boom of 2020-2021 saw a similar level of retail participation, enthusiasm, and price appreciation… for a time. Since 2020, nearly 600 SPACs completed mergers and became public companies, and over 90% trade below their IPO price – with a median return of -87%! Hype and easy access are one thing, fundamentals are very much another.

The optimistic view of the potential IPO boom ahead is that these companies have reached a size and level of importance at which public markets are the most appropriate listing venue. Public markets offer a more diverse and (theoretically) longer-term investor base, while requiring levels of governance, transparency, and oversight that foster trust and legitimacy. The cynical view might be that the private capital pool is nearing saturation, and that AI-adjacent private companies need to go public to fund investments in the business and to allow early investors and employees an easier way to realize gains on their stock.

The truth is likely somewhere in the middle, but the data on IPOs is unambiguous: hype has rarely translated into long-term gains, and the majority of IPOs have been money-losing investments over the longer-term. That doesn’t mean every touted IPO will fail…but it is an argument for caution when excitement runs high.

Disclosures

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Market and economic statistics, unless otherwise cited, are from data provider FactSet.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should not consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

For investment advice specific to your situation, or for additional information, please contact your Baird Financial Advisor and/or your tax or legal advisor.

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Copyright 2026 Robert W. Baird & Co. Incorporated.

Other Disclosures

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.