To Bubble or Not to Bubble: That Is the Question

John:

As you touched on in your most recent blog, Mike, topic No. 1 in the financial media these days is the question of stock market valuations, and whether they presage a painful selloff in 2021.

Famed investor and perma-bear Jeremy Grantham recently published a commentary declaring that we are facing an “epic bubble,” “a bubble that’s beginning to look like a real humdinger,” a bubble evidenced by “extreme overvaluation, explosive price increases, frenzied issuance and hysterically speculative investor behavior.”

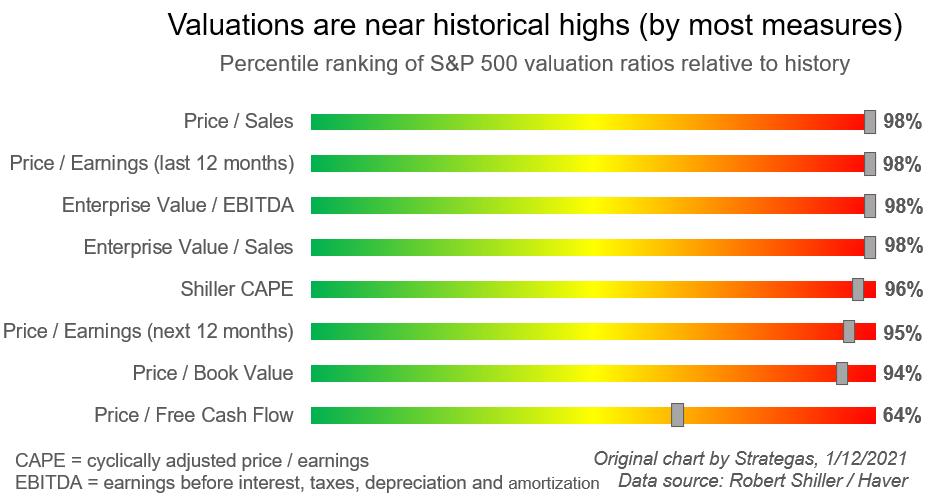

Our own Jason DeSena Trennert, the CEO of Strategas, points out that the S&P 500’s valuation, as a percentage of U.S. and global GDP, rivals pre-tech wreck levels. His colleague Ryan Grabinski posted this chart showing that “looking at the history of various valuation metrics for the S&P 500, virtually every metric is at or near the 100th percentile of their respective histories,” adding, “It’s hard to call the market cheap.”

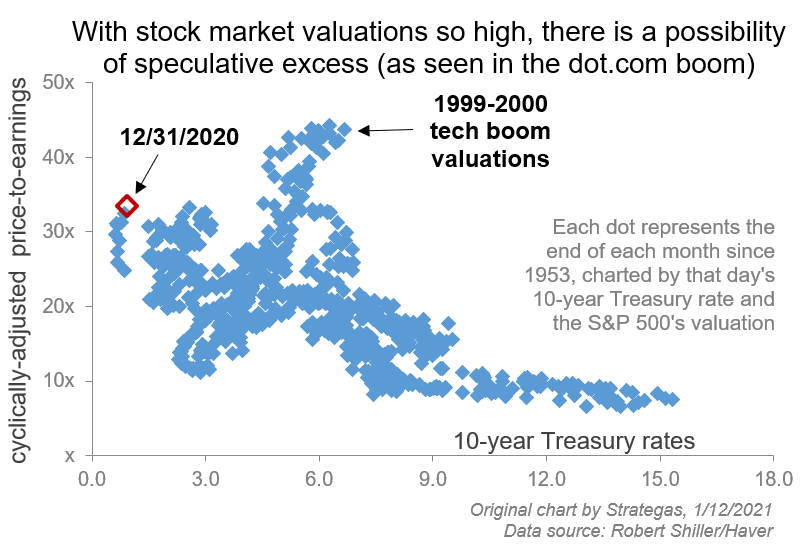

Robert Shiller’s CAPE (cyclically adjusted price-to-earnings ratio) is trading at 33 times the 10-year U.S. Treasury rate, similar to what it was in 2000.

What’s your take? Is this a bubble? And, if so, what if anything can individual investors do about it?

Mike:

Instead of flowery prose, let me get right to the punchline: I think that parts of the market ARE showing signs of excessive speculation, but I don’t think the entire market is a bubble. For example, as I’m writing this, the top five stocks in the S&P 500 are trading at 34 times their 2021 earnings; the bottom 495 are trading at 21 times. Should these top five, which are all tech, trade for a significantly higher multiple based on the kind of company they are? Sure, but that’s also a pretty big disparity.

SPACs (a type of speculative IPO) are multiplying faster than rabbits, retail investors are binging on call options, and for at least a week or so, the hottest stock in the world was a struggling videogame retailer. The atmosphere right now is highly speculative. As our friends at Strategas recently pointed out, more and more people are asking for Google’s thoughts on whether we’re in a bubble. Searches for “stock market bubble” recently hit their highest volume since 2004:

That being said, I don’t think it would be profitable to short the entire S&P 500 because you are worried this is a bubble. If certain sectors of the market (or individual names) look to be out of touch with reality, does that mean Utilities are too? Industrials?

First and foremost, individual investors need to understand what they own and why. What sectors are they in, how much exposure do they have to richly valued stocks, and what would happen if the market corrected those stocks and not others? Don’t wait - ask those questions now.

John:

Thank you for addressing the rubber-meets-the-road conundrum facing investors, Mike: Even if the market is toppy, hedging it is both extraordinarily hard to do and very expensive. Particularly with most portfolios showing large unrealized capital gains, and with cash and bonds (the traditional safe havens) yielding negative real returns.

The best approach is to “anticipate the anticipation of trouble,” as the late Barton Biggs put it, and revisit your asset allocation. How will it perform if the market goes down 20%? 50%? Even 75%? Will you be able to look at your holdings and hang in there? If not, “don’t wait” (as you put it). Now is the time to make adjustments.

Those adjustments should be at the margin, with your “relative bets.” Strategas likes value stocks (which have underperformed for decades) over growth stocks and international stocks over U.S. stocks, and favor placing bets on financial and energy stocks.

What would you do?

Mike:

I am a huge believer in the notion that asset allocation matters more than security selection, so like you said, first I’d want to make sure my stock-to-bond mix is correct for this moment in time and for who I am as an investor.

Then I’d consider what many call a “barbell” approach. It’s OK to have some growth stocks and some value stocks, some companies that benefit from trends in tech and some that benefit from faster economic growth.

There’s also a sector I think has a significant multiyear tailwind to it, housing, that investors could look towards for fresh ideas.

Even if we think that parts of the market are experiencing out of control, rampant speculation, that doesn’t mean you need to abandon investing completely. Remember, you should never be “all in” or “all out” of stocks; that’s a fool’s game. The key to long-term success will always be balance.