Even Now, There Are Reasons To Own Bonds

If you’re like a lot of investors, you’re probably reviewing your fixed income holdings thinking, You had one job! After all, given their traditionally reduced potential for return versus stocks, many investors turn to bonds primarily for diversification – a potential backstop should the equity markets turn sour. So, when both stocks and bonds plummet, as they did in 2022, you could be forgiven for second-guessing your exposure to fixed income. Yet doing so might be underappreciating the true value bonds bring to your portfolio. We spoke with John Craddock, CFA®, Baird Trust’s Director of Fixed Income, and Ross Mayfield, CFA®, Investment Strategy Analyst for Baird Private Wealth Management, about the benefits of fixed income in a down market.

A Historically Challenging Year

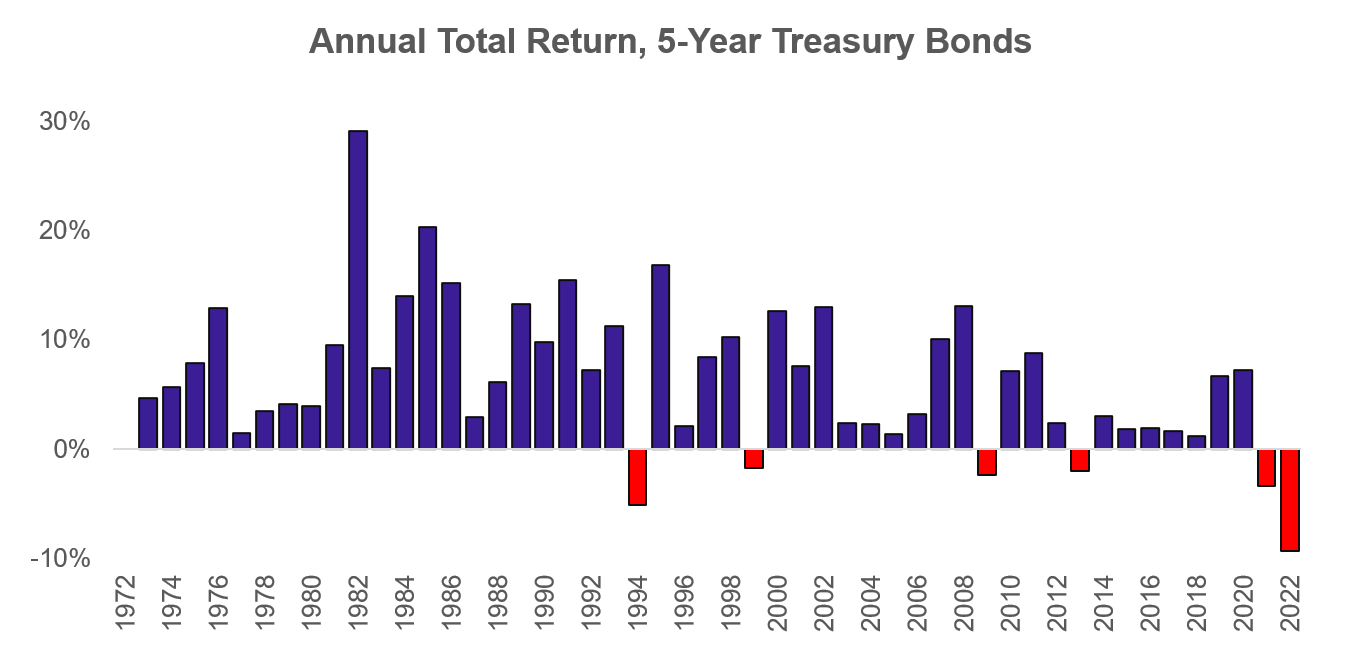

When we talk about bond returns, it’s important to remember that yields and price move opposite one another. That is, when interest rates (yields) are rising, bond prices – all else equal – will fall. For example, the 10-year Treasury yield rose from 1.52% on Dec. 31, 2021, all the way to 3.88% by the end of 2022. While perhaps low in absolute terms (especially vs. the double-digit Treasury yields of the 1980s), this rapid jump shook the bond market to its core: U.S. Treasury bonds had their worst annual return in nearly a century (see Figure 1).

Figure 1. Five-year Treasury bonds had their worst annual total return in decades.

This performance undoubtedly rattled many investors who have depended on their bond portfolio for stability, reliable income and an offset to stock market drops. And while it’s true that making bonds a part of a diversified portfolio typically “smooths the ride” for investors over the long term, there are times, like we witnessed last year, when both bonds and stocks can fall in value. This can lead to investor angst, but it is important to keep in mind some bond basics and how bonds are different from stocks.

Take Comfort in Coupon and Principal Cashflow

As suggested by the term “fixed income,” bonds are essentially a stream of known cashflows, typically consisting of semiannual interest payments and a principal payment at maturity. These cashflows are not affected by the price movement of the bond, and issuers do not have the option to skip or defer payments, as they do with stock dividends. Investors can take comfort knowing that, even with the current price volatility, actual coupon payments will continue to flow, and – short of outright default – the return of principal gets closer each passing day, with no sell transaction required. And the best part? Investors get to reinvest their bond proceeds at the much higher rates we see today.

(It’s worth noting that we’re making a distinction here between individual bonds holdings and bond funds, which are professionally managed pools of bonds. While the two share some of the same potential diversification and yield benefits, bond funds have fluctuating monthly distributions and no maturity date. Importantly, bond funds can increase or decrease in value, much like stocks – in contrast, individual bonds can be held to maturity, at which point 100% of principal value is returned in cash.)

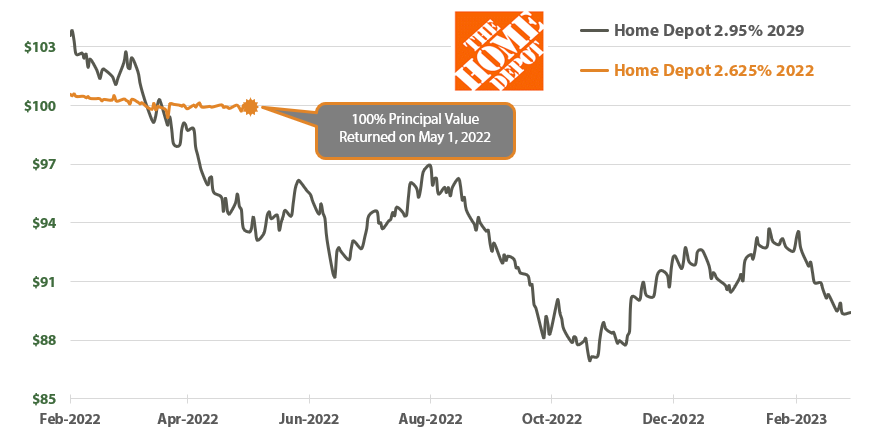

It's also worth revisiting the relationship between time to maturity and price volatility. Figure 2 depicts the recent price movement of two different bonds from the same issuer, one with a 2022 maturity and the other with a 2029 maturity. Throughout its lifecycle, the 2022 Home Depot bond paid all 14 of its coupons and returned 100% of its principal value on May 1. And while the longer 2029 bond has experienced significantly more price volatility than the 2022 bond, it too has continued to pay regular coupons and is on track for 100% principal return – just like its 2022 cousin. As an investor, you can take comfort knowing that price volatility is only temporary. As it nears maturity, the 2029 Home Depot bond will become less sensitive to interest rate moves, allowing it to steadily pull closer to that $100 par value (also known as the face value of the bond).

Figure 2. Bond price volatility and the maturity date effect. Source: Baird Trust, Bloomberg

Time: A Bond Investor’s Best Friend

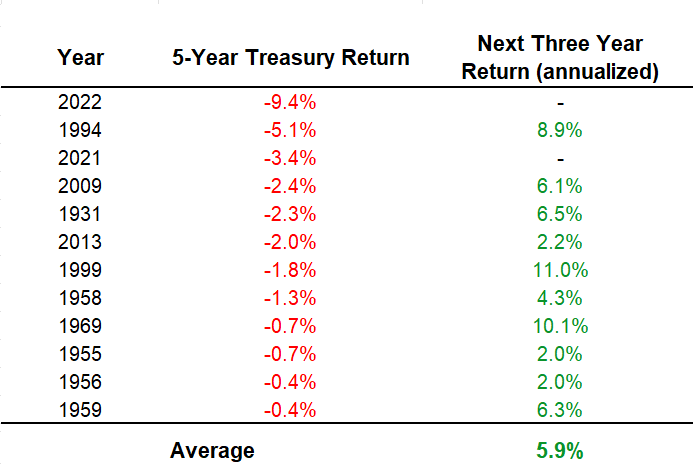

Given the volatile interest rate environment we are experiencing today, never forget the steady coupon flow and “pull to par” of your bond holdings – both are your friend as a bond investor. And while we never welcome a bad year, it does not have to dictate long-term returns. Figure 3 bears witness that bond returns tend to recover strongly in the years following a challenging year: Since 1926, the average return in the three years following a negative year has been right around 6% annually. Not too shabby.

Figure 3. Since 1926, the average annual return in the three years following a negative year has been right around 6%.

In challenging markets like these, it’s easy to question the effectiveness and utility of keeping a healthy exposure of bonds in your portfolio. Just remember that while there are no sure things in investing, each passing day brings bond investors closer to their next semiannual interest payment or return of principal. There’s something to be said about allowing time to be our friend, collecting bond coupons and principal cashflows as we go and reinvesting them at potentially higher rates of return. And with the 10-year Treasury yield hovering around 15-year highs (and shorter-term bonds yielding even more), those potentially higher returns are now a reality after years of rock bottom interest rates and easy monetary policy. Your Baird Financial Advisor would be happy to sit down with you and discuss the role bonds can play in your own portfolio.

Editor’s Note: This article was originally published July 2022 and was updated March 2023 with more current information.

This information has been developed by a member of Baird Wealth Solutions Group, a team of wealth management specialists who provide support to Baird Financial Advisor teams. The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. The information reflected on this page are Baird expert opinions today and are subject to change. The information provided here has not taken into consideration the investment goals or needs of any specific investor and investors should not make any investment decisions based solely on this information. Past performance is not a guarantee of future results. All investments have some level of risk, and investors have different time horizons, goals and risk tolerances, so speak to your Baird Financial Advisor before taking action.